Phoventus celebrates a decade of positive growth for renewables and hybrid power solutions

As Phoventus celebrates its 10th Anniversary, we look back at the extraordinary rise in the use of renewable energy worldwide since we launched our business and ponder the challenges for the sector that lay ahead.

It’s quite extraordinary to reflect back on the dramatic changes we have seen as a business and within the global energy market since Phoventus launched 10 years ago. Back then, the world was still reeling from the shock of the global financial crisis in 2008. Then, meaningful international action to curb the rise in greenhouse gas emissions and ensure more sustainable supplies of energy for all was still up for debate. At the same time, more than 1 billion people in the world remained without access to electricity at all.

With years of austerity ahead, the then Executive Director of the International Energy Agency (IEA), Nobuo Tanaka, issued a warning. “We cannot let the financial and economic crisis delay the policy action urgently needed to ensure secure energy supplies and to curtail rising emissions of greenhouse gases.” Launching the IEA’s World Energy Outlook (WEO) 2008, he said: “We must usher in a global energy revolution by improving energy efficiency and increasing the deployment of low-carbon energy.”

Perhaps to many people’s surprise, that is precisely what happened. Whilst there is still much work to do, the rise of key renewable energy technologies – such as solar PV and wind – to become the mainstream power sources they are today has been nothing short of revolutionary. Furthermore, something happened for the first time ever. The total number of people without access to electricity has fallen below 1 billion in the last year.

Phoventus plays an important part

Here at Phoventus, where our consultancy specializes in renewables and hybrid power solutions, we pride ourselves on playing our small part in the energy revolution. We share those same goals Tanaka spoke about as he launched the 2008 WEO all those years ago. The 2018 update of the IEA’s flagship WEO publication (published last November) and its earlier report, Renewables 2018 (published in October), clearly show how far the world has come. This is all thanks to some extraordinary political will and technological innovation over the last decade.

From growing electrification to the expansion of renewables, “major transformations are underway”, says WEO 2018. Today, we live in a world where onshore wind power and solar PV are cost-competitive with fossil fuels in some parts of the world. In fact, since 2010, the cost of new installations has been reduced by 70% for solar PV and 25% for wind. Moreover, their share of the global power market continues to rise beyond expectation.

Strong outlook

Whilst coal and gas still dominate supply, renewables now account for 25% of the world’s power generation mix. In 2023, the IEA expects renewables to account for almost a third of world electricity generation. Also, by 2040, the share of renewables in power generation should rise to over 40%. This is under the New Policies Scenario (NPS) in WEO 2018. “In power markets, renewables have become the technology of choice, making up almost two-thirds of global capacity additions to 2040, thanks to falling costs and supportive government policies,” says the IEA in WEO 2018. “This is transforming the global power mix.”

Others are even bolder in their projections. For example, in its New Energy Outlook 2018 report, Bloomberg New Energy Finance (NEF) suggests wind and solar alone will together provide 48% of the world’s electricity by 2050. “Wind and solar are set to surge to almost “50 by 50” – 50% of world generation by 2050 – on the back of precipitous reductions in cost, and the advent of cheaper and cheaper batteries that will enable electricity to be stored and discharged to meet shifts in demand and supply. Coal shrinks to just 11% of global electricity generation by 2050.”

What’s the forecast?

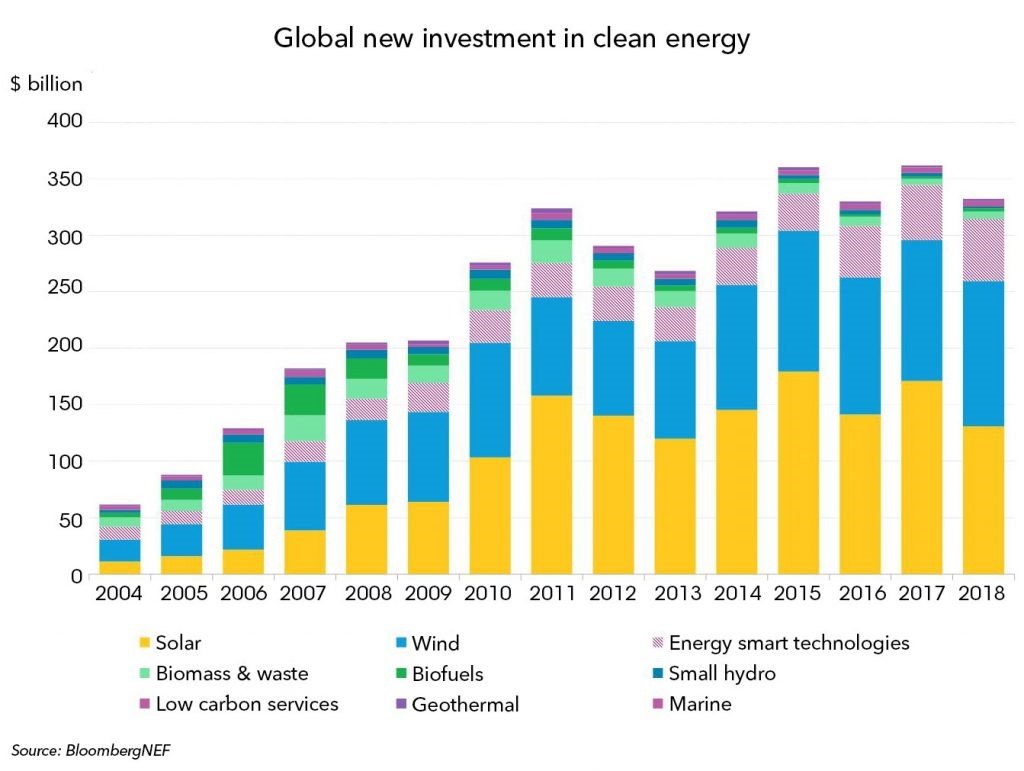

It forecasts some $11.5 trillion being invested globally in new power generation capacity between 2018 and 2050. Interestingly, $8.4 trillion of that will go to wind and solar. Another $1.5 trillion will go to other zero-carbon technologies such as hydro and nuclear. This investment will produce a 17-fold increase in solar photovoltaic capacity worldwide. And, it will also produce a six fold increase in wind power capacity. The levelized cost of electricity (LCOE) from new PV plants is forecast by Bloomberg NEF to fall a further 71% by 2050. On the other hand, that for onshore wind will drop by a further 58%.

These two technologies have already seen LCOE reductions of 77% and 41% respectively between 2009 and 2018. “Beaten on cost by wind and PV for bulk electricity generation, and batteries and gas for flexibility, the future electricity system will reorganize around cheap renewables – coal gets squeezed out.” This is what the company’s head of energy economics, Elena Giannakopoulou said.

Growth markets

The 178 gigawatts (GW) of renewable capacity additions in 2017 broke another record. It accounted for more than two-thirds of global net electricity capacity growth for the first time, notes the IEA. Solar PV capacity expanded the most (97 GW), over half of which was in China. Meanwhile, although markets remain strong, onshore wind additions globally declined for the second year in a row. And, hydropower growth continued to decelerate.

Over the five years to end 2023, IEA expects renewable capacity to grow by over 1 TW (46%). This is under prevailing market and policy conditions. Solar PV capacity will account for more than half of this expansion, with almost 600 GW added. Despite recent policy changes, China remains the absolute solar PV leader by far. It holds almost 40% of global installed PV capacity in 2023. The United States remains the second-largest growth market for solar PV. India, whose capacity quadruples, comes in third.

What do the experts expect?

Wind will remain the second-largest contributor to renewable capacity growth. In addition, hydropower will still be the largest renewable electricity source by 2023. The experts expect wind capacity to expand by 60% (324 GW to reach a cumulative total of 839 GW). This is with offshore wind accounting for 10% of that growth (with cumulative capacity tripling to 52 GW). Meanwhile, spurred by technological progress and significant cost reductions, onshore wind capacity triples. Its growth continues to move beyond Europe to Asia and North America. The Renewables 2018 report adds that if governments were to introduce some market and policy enhancements before 2020, the growth in renewable capacity to 2023 could be 25% higher (reaching 1.3 TW). This means, therefore, we can expect annual additions for solar PV to be in the 110 – 140 GW region. And, onshore wind at around 50 – 60 GW, it says.

In terms of markets, China has become the powerhouse for renewables growth. The IEA expects it to become the largest consumer of renewable energy, surpassing the European Union by 2023. Of the world’s largest energy consumers, Brazil, has the highest share of renewables by far. It has almost 45% of total final energy consumption in 2023. It was driven by significant contribution of bioenergy and hydropower.

Global electrification

Importantly, there has been a marked growth in rural electrification. Off-grid and hybrid power solutions development helped reduce the number of people without access to electricity significantly. India has completed the electrification of all of its villages. Furthermore, many other Asian countries have also seen significant progress. The IEA analysis also shows that the electrification rate in Indonesia is almost at 95%, up from 50% in 2000. In Bangladesh, 80% of the population has access to electricity, up from 20% in 2000.

Progress has also been made in Africa, with Kenya and Ethiopia proving particularly successful so far. In Kenya access has increased from just 8% in 2000 to 73% today (aiming for universal access by 2022). Additionally, in Ethiopia, access is up from 5% in 2000 to 45% (aiming for universal access by 2025, with 35% of the population served by off-grid solutions).

Is there a reason to be optimistic?

Nonetheless, the IEA points out that the world still remains off-track in its efforts to achieve Sustainable Development Goal (SDG) 7.1 to ensure universal access to affordable, reliable and modern energy services by 2030. In sub-Saharan Africa, 600 million people are without access to electricity, equivalent to 57% of the population. In that region, 15 countries still have access rates below 25%. Meanwhile, 350 million people lack access in developing Asia (9% of the population). In addition, the IEA says nearly 2.7 billion people lack access to clean cooking facilities worldwide. They rely instead on biomass, coal or kerosene as their primary cooking fuel.

But, there is every reason to be optimistic. As we know here at Phoventus, with the technology for off-grid hybrid power projects (featuring renewables and/or energy storage solutions) becoming more effective and less costly day-by-day, the wave of positive change seen in the last decade looks set to continue. Companies that operate in remote regions – such as those running mining operations – are now increasingly turning to hybrid power. They do it to secure their energy supplies, boost operational efficiency, and reduce their overall running costs. With this, we often see the benefits spread beyond their direct operational borders and into nearby villages. And, this trend is likely to continue.

Battery breakthroughs

Development in battery energy storage and demand side response technology is now a key focus of energy industry innovators. This is especially important for rural electrification and for wider scale use in traditional utility power networks. Moreover, it will be critical as the world continues to increase its use of renewables. “Flexibility will be the cornerstone of future electricity systems,” says IEA’s Claudia Pavarini, a WEO energy analyst. “New sources of flexibility, including battery storage and demand-side response, are projected to grow fast. They will contribute 400 GW by 2040.”

As she points out, battery storage systems are modular and allow a wide range of applications. “As costs continue to fall, installations have tripled in less than three years. They are largely driven by lithium ion batteries – mostly aimed at providing short-term storage. And, they now account for just over 80% of all battery capacity. For applications with longer storage durations other battery types, including sodium sulfur and in particular flow batteries, are attracting increased interest. Small-scale battery storage is also making inroads. In off-grid solar applications for energy access, the vast majority of systems now include a storage unit.”

What about the cost?

Further cost declines for battery storage systems are about to happen, says Pavarini. She notes that costs for four-hour battery systems are projected to fall to $220 per kWh by 2040 in the NPS. “Together with appropriate market design that rewards these flexible assets, these falling costs are projected to drive the strong deployment of batteries. This includes utility-scale deployment reaching 220 GW by 2040 in the NPS. Most battery additions are expected to be paired with solar PV and wind power as they increase their dispatchability. It will allow revenue stacking from energy arbitrage and ancillary services offered to the grid.”

Bloomberg NEF concurs. Its NEO 2018 report highlights the “huge impact” falling battery costs will have on the electricity mix over the coming decades. It predicts that lithium-ion battery prices, already down by nearly 80% per megawatt-hour since 2010, will continue to tumble as electric vehicle manufacturing builds up through the 2020s. “We see $548 billion being invested in battery capacity by 2050. It includes two thirds of that at the grid level. And, one third installed behind-the-meter by households and businesses.” Seb Henbest, head of Europe, Middle East and Africa for BNEF and lead author of NEO 2018 said that. “The arrival of cheap battery storage will mean that it becomes increasingly possible to finesse the delivery of electricity from wind and solar. This is so these technologies can help meet demand even when the wind isn’t blowing and the sun isn’t shining.

The result will be renewables eating up more and more of the existing market for coal, gas and nuclear.”

Political lead

The incredible energy transition that has got underway in the last ten years has been spurred on by positive policy action by governments worldwide in the wake of international climate change agreements. This started with the Copenhagen Accord (a global agreement to try to limit global temperature rises to 2oC). It was signed in December 2009 followed some years later by the more concrete goals in the 2015 Paris Agreement. It came into force in 2016 and sets the ambitious goal of limiting global warming to well below 2°C. At the same time, it is pursuing efforts to limit the increase to 1.5°C.

But, ten years after Tanaka issued his 2008 warning, his successor at the IEA, Dr. Fatih Birol, has also called on political leaders to remain focused and proactive amidst difficult economic conditions. As he launched WEO 2018, Dr. Birol was firm: “The world’s energy destiny lies with government decisions”. Whilst solar PV and wind are charging ahead, other low-carbon technologies and especially efficiency policies “still require a big push”, he said. Across all regions and fuels, policy choices made by governments will determine the shape of the energy system of the future. “Crafting the right policies and proper incentives will be critical to meeting our common goals of securing energy supplies, reducing carbon emissions, improving air quality in urban centers, and expanding basic access to energy in Africa and elsewhere,” Dr. Birol said.

What’s to come?

Going forward, higher electrification in transportation, buildings and industry, whilst leading to a peak in oil demand by 2030 and reducing harmful local pollutants, would have a negligible impact on carbon emissions without stronger efforts to increase the share of renewables and low-carbon sources of power, says the IEA. At the same time, the rapid growth of disruptive renewable energy technologies brings challenges that policy makers “need to address quickly”, Dr. Birol said.

With higher variability in supplies, power systems will need to “make flexibility the cornerstone of future electricity markets in order to keep the lights on”. The IEA says the issue is of growing urgency as countries around the world quickly ramp up their share of solar PV and wind. It will require “market reforms, grid investments, as well as improving demand-response technologies. Some of them include smart meters and battery storage technologies”.

Is the New Policies Scenario good enough?

Dr. Birol and his team of IEA analysts behind the WEO make one other key thing clear. For the world to achieve the objectives of the Paris Agreement on climate change, the New Policies Scenario is not good enough. “We have reviewed all current and under-construction energy infrastructure around the world. This includes power plants, refineries, cars and trucks, industrial boilers, and home heaters. They will account for some 95% of all emissions permitted under international climate targets in coming decades,” said Dr Birol. In fact, IEA analysis published in December shows the world’s advanced economies saw an uptick in their carbon dioxide emissions in 2018, bucking a five year-long decline.

“This means that if the world is serious about meeting its climate targets then, as of today, there needs to be a systematic preference for investment in sustainable energy technologies. But, we also need to be much smarter about the way that we use our existing energy system. We can create some room for manoeuvre by expanding the use of Carbon Capture Utilization and Storage, hydrogen. We can also do it by improving energy efficiency, and in some cases, retiring capital stock early.”

The IEA’s prognosis

The IEA’s Sustainable Development Scenario offers a pathway to meeting various climate, air quality and universal access goals in an integrated way. In this scenario, global energy-related CO2 emissions peak around 2020. Then, they enter a steep and sustained decline, fully in line with the trajectory required to achieve the objectives of the Paris Agreement on climate change. “To be successful, this will need an unprecedented global political and economic effort,” said Dr. Birol.

As we enter our second decade of business, all of us here at Phoventus look forward to playing our role in achieving that success.